May 19, 2026

What Happens If You Default on an Unsecured Business Loan?

What lenders can actually do when a business cannot repay an unsecured business loan, and whether your personal assets are at risk.

Business Lending

Unsecured Business Loans

Business Finance

What Is An Unsecured Business Loan?

An unsecured business loan is finance provided without specific business assets being taken as direct security. Instead of relying on equipment or property, lenders assess factors like revenue, cash flow, trading history and credit profile to determine risk.

Unsecured business loans are commonly used for working capital, growth, payroll, tax debt, inventory and short-term cash flow support. Because there is no registered asset attached to the facility, approval times are often faster than traditional secured lending.

That speed and flexibility also means many business owners ask an important question before applying:

“What actually happens if I cannot repay it?”

The answer depends on:

whether a personal guarantee was signed

the lender’s recovery process

the structure of the business

how early communication happens when financial pressure appears

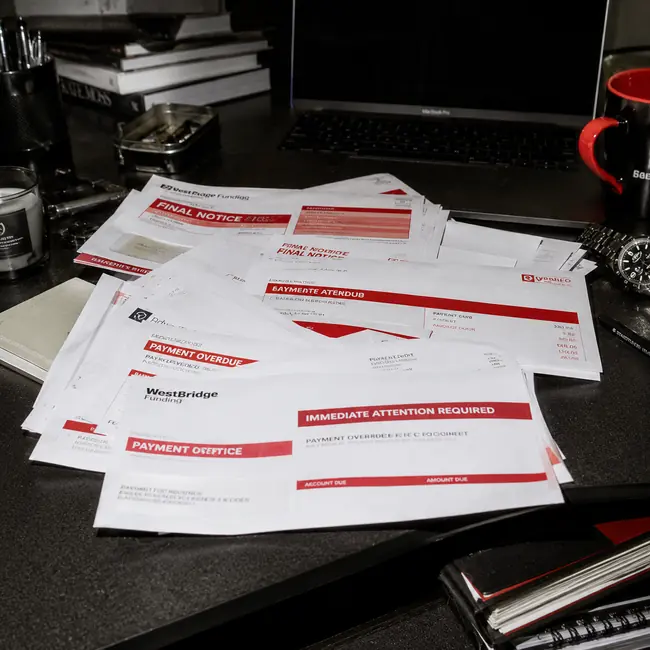

Default does not automatically mean someone turns up and takes your house. But lenders do have legal recovery pathways available depending on the agreement signed at settlement.

Can A Lender Take Your House?

This is one of the most searched questions around unsecured business loans in Australia, and the answer is: sometimes, but not automatically.

Most unsecured business loans still involve some form of personal guarantee from the director or borrower. A personal guarantee means the lender may pursue the guarantor personally if the business cannot repay the debt.

That does not mean immediate repossession.

In practice, lenders usually follow a staged recovery process:

missed payment reminders

hardship discussions

repayment restructuring

collections activity

legal enforcement only if unresolved

Whether personal assets become exposed depends heavily on:

the wording of the guarantee

whether legal judgement occurs

the borrower’s financial position

whether secured assets exist elsewhere

Many lenders prefer negotiated repayment outcomes over aggressive enforcement. Recovering funds through litigation is expensive and time consuming for both sides.

What Do Lenders Usually Do After Default?

Most lenders focus on recovery and resolution before pursuing formal legal action.

When a business defaults on an unsecured business loan, lenders typically begin with internal collections and hardship engagement.

The earlier a borrower communicates, the more options usually remain available.

Possible outcomes may include:

revised repayment plans

short-term pauses

refinancing

debt restructuring

negotiated settlements

If communication stops completely, the matter may escalate to external collections, default listings or legal proceedings.

For business owners, the most important step is usually early action rather than avoidance. Ignoring the issue generally reduces flexibility and increases financial pressure over time.

Not all defaults end in insolvency or litigation. Many are resolved commercially through restructuring or negotiated repayment arrangements.

Let's Work Together

Contact Us

Contact Now

Let's get you Funded

Tell us what you need, how much, and how soon. We’ll show you what’s actually possible.

Australian based team. Multiple Lenders, more options

FAQ

01

What types of business loans do you offer?

02

How quickly can I get approved?

03

What if I am unsure which loan I need?

04

What do I need to apply?

05

Will this affect my credit score?

06

I’ve been declined before. Can you still help?

07

How much can I borrow?

08

How are repayments structured?

No credit check. No jargon. Just a number.

Get a Loan →Capioo Pty Ltd acts as an introducer and referral partner for finance products and services. We are not a lender and do not provide financial or credit advice. All applications are subject to lender assessment, eligibility criteria and approval. Terms, conditions, fees and charges may apply.

May 19, 2026

What Happens If You Default on an Unsecured Business Loan?

What lenders can actually do when a business cannot repay an unsecured business loan, and whether your personal assets are at risk.

Business Lending

Unsecured Business Loans

Business Finance

What Is An Unsecured Business Loan?

An unsecured business loan is finance provided without specific business assets being taken as direct security. Instead of relying on equipment or property, lenders assess factors like revenue, cash flow, trading history and credit profile to determine risk.

Unsecured business loans are commonly used for working capital, growth, payroll, tax debt, inventory and short-term cash flow support. Because there is no registered asset attached to the facility, approval times are often faster than traditional secured lending.

That speed and flexibility also means many business owners ask an important question before applying:

“What actually happens if I cannot repay it?”

The answer depends on:

whether a personal guarantee was signed

the lender’s recovery process

the structure of the business

how early communication happens when financial pressure appears

Default does not automatically mean someone turns up and takes your house. But lenders do have legal recovery pathways available depending on the agreement signed at settlement.

Can A Lender Take Your House?

This is one of the most searched questions around unsecured business loans in Australia, and the answer is: sometimes, but not automatically.

Most unsecured business loans still involve some form of personal guarantee from the director or borrower. A personal guarantee means the lender may pursue the guarantor personally if the business cannot repay the debt.

That does not mean immediate repossession.

In practice, lenders usually follow a staged recovery process:

missed payment reminders

hardship discussions

repayment restructuring

collections activity

legal enforcement only if unresolved

Whether personal assets become exposed depends heavily on:

the wording of the guarantee

whether legal judgement occurs

the borrower’s financial position

whether secured assets exist elsewhere

Many lenders prefer negotiated repayment outcomes over aggressive enforcement. Recovering funds through litigation is expensive and time consuming for both sides.

What Do Lenders Usually Do After Default?

Most lenders focus on recovery and resolution before pursuing formal legal action.

When a business defaults on an unsecured business loan, lenders typically begin with internal collections and hardship engagement.

The earlier a borrower communicates, the more options usually remain available.

Possible outcomes may include:

revised repayment plans

short-term pauses

refinancing

debt restructuring

negotiated settlements

If communication stops completely, the matter may escalate to external collections, default listings or legal proceedings.

For business owners, the most important step is usually early action rather than avoidance. Ignoring the issue generally reduces flexibility and increases financial pressure over time.

Not all defaults end in insolvency or litigation. Many are resolved commercially through restructuring or negotiated repayment arrangements.

Let's Work Together

Contact Us

Contact Now

Let's get you Funded

Tell us what you need, how much, and how soon. We’ll show you what’s actually possible.

Australian based team. Multiple Lenders, more options

FAQ

01

What types of business loans do you offer?

02

How quickly can I get approved?

03

What if I am unsure which loan I need?

04

What do I need to apply?

05

Will this affect my credit score?

06

I’ve been declined before. Can you still help?

07

How much can I borrow?

08

How are repayments structured?

No credit check. No jargon. Just a number.

Get a Loan →Capioo Pty Ltd acts as an introducer and referral partner for finance products and services. We are not a lender and do not provide financial or credit advice. All applications are subject to lender assessment, eligibility criteria and approval. Terms, conditions, fees and charges may apply.

May 19, 2026

What Happens If You Default on an Unsecured Business Loan?

What lenders can actually do when a business cannot repay an unsecured business loan, and whether your personal assets are at risk.

Business Lending

Unsecured Business Loans

Business Finance

What Is An Unsecured Business Loan?

An unsecured business loan is finance provided without specific business assets being taken as direct security. Instead of relying on equipment or property, lenders assess factors like revenue, cash flow, trading history and credit profile to determine risk.

Unsecured business loans are commonly used for working capital, growth, payroll, tax debt, inventory and short-term cash flow support. Because there is no registered asset attached to the facility, approval times are often faster than traditional secured lending.

That speed and flexibility also means many business owners ask an important question before applying:

“What actually happens if I cannot repay it?”

The answer depends on:

whether a personal guarantee was signed

the lender’s recovery process

the structure of the business

how early communication happens when financial pressure appears

Default does not automatically mean someone turns up and takes your house. But lenders do have legal recovery pathways available depending on the agreement signed at settlement.

Can A Lender Take Your House?

This is one of the most searched questions around unsecured business loans in Australia, and the answer is: sometimes, but not automatically.

Most unsecured business loans still involve some form of personal guarantee from the director or borrower. A personal guarantee means the lender may pursue the guarantor personally if the business cannot repay the debt.

That does not mean immediate repossession.

In practice, lenders usually follow a staged recovery process:

missed payment reminders

hardship discussions

repayment restructuring

collections activity

legal enforcement only if unresolved

Whether personal assets become exposed depends heavily on:

the wording of the guarantee

whether legal judgement occurs

the borrower’s financial position

whether secured assets exist elsewhere

Many lenders prefer negotiated repayment outcomes over aggressive enforcement. Recovering funds through litigation is expensive and time consuming for both sides.

What Do Lenders Usually Do After Default?

Most lenders focus on recovery and resolution before pursuing formal legal action.

When a business defaults on an unsecured business loan, lenders typically begin with internal collections and hardship engagement.

The earlier a borrower communicates, the more options usually remain available.

Possible outcomes may include:

revised repayment plans

short-term pauses

refinancing

debt restructuring

negotiated settlements

If communication stops completely, the matter may escalate to external collections, default listings or legal proceedings.

For business owners, the most important step is usually early action rather than avoidance. Ignoring the issue generally reduces flexibility and increases financial pressure over time.

Not all defaults end in insolvency or litigation. Many are resolved commercially through restructuring or negotiated repayment arrangements.

Let's Work Together

Contact Us

Contact Now

Let's get you Funded

Tell us what you need, how much, and how soon. We’ll show you what’s actually possible.

Australian based team. Multiple Lenders, more options

FAQ

What types of business loans do you offer?

How quickly can I get approved?

What if I am unsure which loan I need?

What do I need to apply?

Will this affect my credit score?

I’ve been declined before. Can you still help?

How much can I borrow?

How are repayments structured?

No credit check. No jargon. Just a number.

Get a Loan →Capioo Pty Ltd acts as an introducer and referral partner for finance products and services. We are not a lender and do not provide financial or credit advice. All applications are subject to lender assessment, eligibility criteria and approval. Terms, conditions, fees and charges may apply.